Lifetime financial security isn’t just a buzzword — it’s a priority, especially for older adults in New York. Senior life insurance NY helps you protect loved ones, cover final expenses, and leave a legacy without leaving financial burdens behind.

Many seniors delay coverage because they think it’s too expensive or no longer necessary. However, the right policy can be affordable, simple, and tailored to your needs — especially when you know what to compare and what questions to ask.

Meta description: Discover how senior life insurance works in New York, affordable options for older adults, and how to choose the right policy with real examples and smart tips.

Why Senior Life Insurance Still Matters in NY

As you grow older, some financial risks change but don’t go away. Life insurance for seniors often focuses on:

- paying final expenses (funeral, medical bills)

- leaving money to family or loved ones

- covering remaining debts

- supporting a legacy or charitable goals

For example, a 65-year-old New Yorker may not have dependents but wants to ensure their spouse or children aren’t left with unexpected funeral costs. A small policy can take that burden off their shoulders.

Types of Senior Life Insurance Available

When seniors shop for life insurance in NY, there are a few main options worth understanding:

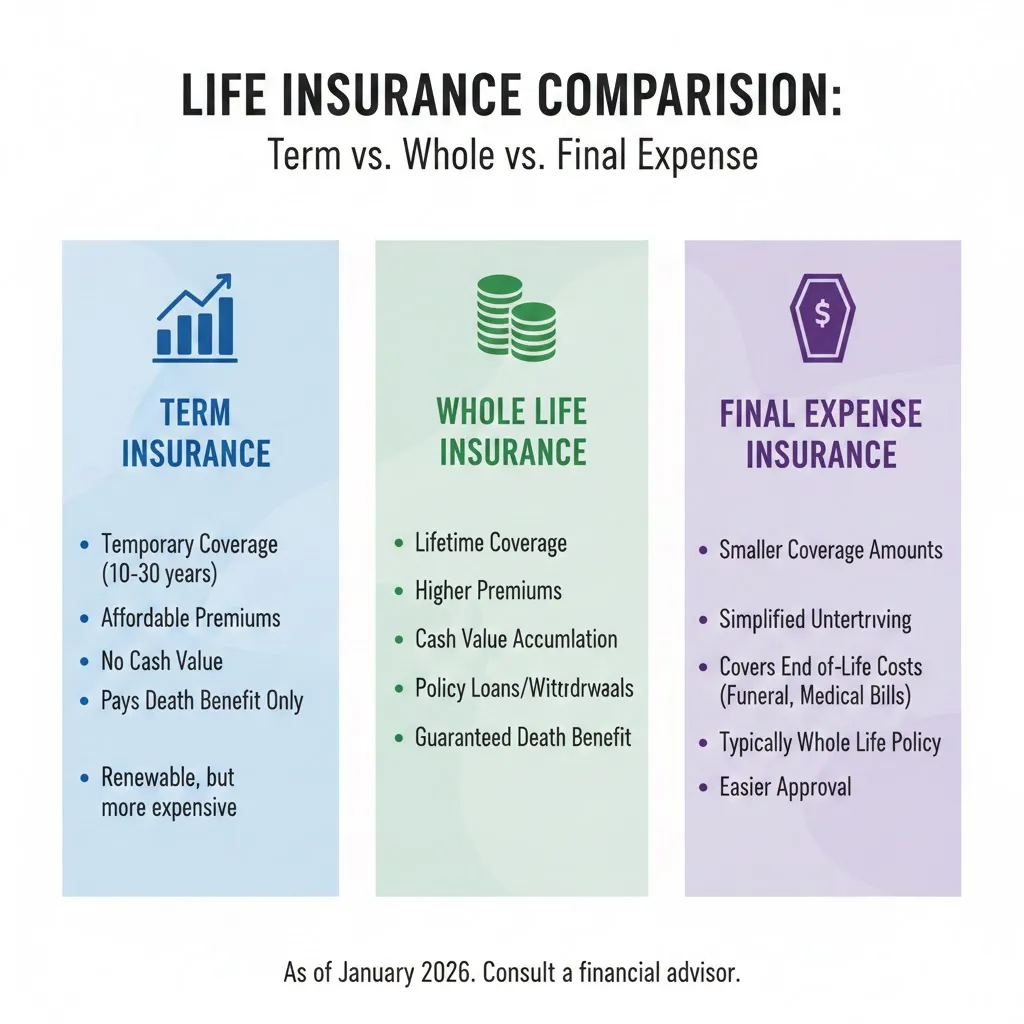

Term Life Insurance

Covers a set number of years and is generally cheaper — but may not last a lifetime.

Whole Life Insurance

Provides lifelong coverage and includes a cash value component, which grows over time.

Guaranteed Universal Life (GUL)

Combines affordability with long-term coverage — a popular choice for seniors who want predictable premiums without complex investing.

Final Expense Insurance

Designed specifically to cover funeral and related costs. Policies are smaller and easier to qualify for.

Senior buyers often start with a clear estimate of their financial needs — this helps match the right policy type. If you want cost comparisons for different ages, reviewing a life insurance quotes guide can be useful.

What Affects Your Life Insurance Cost in NY

Senior life insurance quotes can vary a lot based on:

- age

- health history

- smoking status

- the type of policy

- coverage amount

In New York, insurers follow state regulations, but each company still sets its own prices. For example, a healthy 60-year-old may pay much less for whole life insurance than someone at 70 with mild health conditions.

Higher coverage and longer terms cost more, but many seniors find that modest coverage tailored to their needs fits comfortably in their budget.

Comparison: Senior Policy Choices

| Feature | Term Life | Whole Life | Final Expense |

|---|---|---|---|

| Lifetime coverage | No | Yes | Yes |

| Premium predictability | Moderate | High | Moderate |

| Cash value | No | Yes | Limited |

| Best for | Short-term needs | Lifelong protection | Funeral / small legacy |

| Typical cost | Lower | Higher | Moderate–Low |

This table can help you decide which policy fits your priorities — whether it’s affordability, lifetime protection, or simplicity.

How to Choose the Right Policy as a Senior

Choosing life insurance after age 50 is less about “one size fits all” and more about your personal goals.

Here are key questions to consider:

Why do you want coverage?

Is it for funeral costs, family legacy, or debt protection?

How much can you afford monthly?

A clear budget helps narrow your options.

Do you want guaranteed acceptance?

Guaranteed plans may cost slightly more, but you won’t be declined for health issues.

How long do you want coverage to last?

Term can be cheaper if you only need coverage for a certain period, while whole life covers you forever.

Speaking with a licensed agent in NY can refine these answers and match you with the right plan.

Common Mistakes Seniors Should Avoid

Many seniors could save money or get better coverage by avoiding these missteps:

- choosing too much coverage for needs

- skipping comparisons across insurers

- assuming “no medical exam” is always cheaper

- ignoring riders that can add value (like accelerated death benefit)

A financial planning checklist helps ensure you focus on goals, not just premiums.

Pro Insight

Many seniors underestimate the value of guaranteed universal life (GUL) policies because they combine lifelong protection with lower premiums than traditional whole life — making them a strong choice for those who want predictability.

Quick Tip

Always compare quotes from multiple insurers at the same time using the same coverage amount and term — this creates an accurate apples-to-apples comparison before you buy.

FAQs About Senior Life Insurance in NY

Can seniors get life insurance at age 70 or older?

Yes. Many insurers offer coverage into later ages, but options vary by health and provider.

Is a medical exam always required?

Not always. Some plans offer no-exam options, though they may cost more.

What is guaranteed acceptance insurance?

Policies that don’t require health questions — often used by older buyers with health challenges.

Can life insurance help cover final expenses?

Yes — final expense plans are designed specifically for that purpose.

Do premiums stay level for life?

Whole life and many guaranteed policies have level premiums, while term can increase if renewed later.

Disclaimer

This article is for general informational purposes only and does not provide financial, legal, or insurance advice. Coverage, pricing, and eligibility vary by insurer and individual circumstances.